Credit cards used to be simple.

You spent money.

You paid it back.

End of story.

Today, credit cards are something very different. They are marketing machines, loyalty tools, and—when used correctly—quiet financial advantages. Cash back and rewards credit cards now promise free money, travel perks, luxury experiences, and bonuses that seem almost too good to be true.

And here’s the truth: many of them aren’t tricks.

But they aren’t free either.

This article breaks down how cash back and rewards credit cards really work, why the offers look so irresistible, and how smart users extract value without falling into expensive traps.

Why Credit Card Rewards Exist at All

Credit card companies don’t give away money out of generosity.

Rewards exist because:

- Card issuers earn interchange fees from merchants

- They profit from interest paid by some users

- Loyal customers are more valuable long-term

Rewards are a calculated expense—not a loss.

When you understand that, the game becomes clearer.

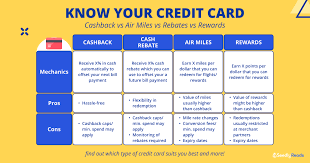

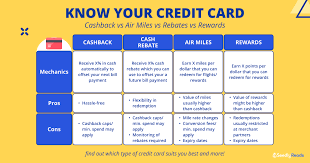

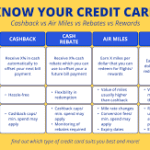

Cash Back Cards: Simple, Transparent, Powerful

Cash back credit cards are the most straightforward reward structure.

You spend money.

You get a percentage back.

Common cash back structures include:

- Flat-rate cash back (e.g., 1.5%–2% on all purchases)

- Category-based bonuses (groceries, gas, dining)

- Rotating quarterly rewards

The appeal is obvious: cash back is flexible, predictable, and easy to value.

One dollar back is always worth one dollar.

Rewards Cards: Points, Miles, and Perks

Rewards cards trade simplicity for potential upside.

Instead of cash, you earn:

- Points

- Miles

- Travel credits

- Statement perks

When used strategically, rewards can unlock:

- Free flights

- Hotel stays

- Upgrades

- Lounge access

When used poorly, they become confusing numbers that never get redeemed.

Value depends entirely on how—and if—you use them.

The Psychology Behind “Offers You Can’t Refuse”

Sign-up bonuses are designed to trigger urgency.

“Spend $3,000 in three months.”

“Earn 60,000 bonus points.”

“Limited-time offer.”

These incentives work because they:

- Encourage higher short-term spending

- Create emotional commitment

- Make people rationalize purchases

The reward isn’t dangerous.

Unplanned spending is.

When Cash Back Beats Rewards Every Time

For many people, cash back is objectively better.

Cash back wins when:

- Spending is consistent but not strategic

- Travel is infrequent

- Simplicity matters

- You want guaranteed value

There is no learning curve and no redemption risk.

Cash back doesn’t expire quietly or lose value overnight.

When Rewards Cards Make Sense

Rewards cards shine for users who:

- Travel regularly

- Understand redemption rules

- Plan spending intentionally

- Pay balances in full

In these cases, rewards can far exceed cash back—sometimes dramatically.

But rewards only outperform cash back when discipline is present.

The Real Cost: Interest Destroys All Rewards

This is the part many people ignore.

If you carry a balance, interest charges quickly erase:

- Cash back earned

- Points accumulated

- Bonus value

One month of interest can undo an entire year of rewards.

Rewards cards are designed for people who do not pay interest.

Everyone else is subsidizing them.

Fees: The Silent Deal Breaker

Some of the most attractive cards come with annual fees.

Fees can be worth it—but only if:

- Benefits exceed the cost

- You actually use the perks

- The card matches your lifestyle

A $95 fee for unused benefits is not a premium experience.

It’s wasted money.

How Executives and High Earners Use Rewards Strategically

Professionals don’t chase every offer.

They focus on:

- Spending alignment

- Value per dollar

- Redemption efficiency

- Minimal account complexity

Their goal isn’t excitement.

It’s optimization.

Rewards are treated as a byproduct—not a motivation.

The CEO Mindset: Rewards Should Reduce Costs, Not Increase Them

Smart decision-makers never spend more just to earn rewards.

They understand:

- Spending is the real cost

- Rewards are secondary

- Control beats accumulation

If a card changes your behavior negatively, it’s not a benefit—it’s a liability.

Common Mistakes Cardholders Make

- Overspending to chase bonuses

- Carrying balances “temporarily”

- Forgetting redemption rules

- Paying fees for unused perks

- Opening too many cards too fast

Credit cards reward attention—not neglect.

How to Choose the Right Card for You

Ask yourself:

- Do I want simplicity or optimization?

- Do I pay my balance in full every month?

- Do I travel enough to justify rewards?

- Will I use the benefits consistently?

The best card is not the most advertised one.

It’s the one that fits your behavior.

Final Thoughts: Yes, the Offers Are Real—If You Play It Right

Cash back and rewards credit cards can be powerful tools.

Used correctly, they:

- Reduce everyday costs

- Add flexibility

- Improve financial efficiency

Used carelessly, they:

- Increase spending

- Add fees

- Create long-term debt

The offers may look irresistible—but the real advantage belongs to those who stay disciplined.

Earn rewards on your terms.

Pay no interest.

And let the system work for you—not against you.

End of article.

Summary:

The competition to get your credit card business has heated up so extensively that banks are literally paying you to take a credit card from them. Nearly every major issuing bank now offers a credit card that gives you bonuses for using their card. Consider the following offers you can find today on Internet sites where you can apply for a card online.

Cash Back Credit Cards

These cards return money to you in the form of checks. Many of the cards offer deals like 5% c…

Keywords:

cash back credit card, credit card, credit card offer, offers, rewards, reward credit card

Article Body:

The competition to get your credit card business has heated up so extensively that banks are literally paying you to take a credit card from them. Nearly every major issuing bank now offers a credit card that gives you bonuses for using their card. Consider the following offers you can find today on Internet sites where you can apply for a card online.

Cash Back Credit Cards

These cards return money to you in the form of checks. Many of the cards offer deals like 5% cash back on purchases at grocery stores, drug stores, and gas stations. In most cases, the stores are the major chains where you probably shop anyway. On top of that, these cash back cards usually offer 1% cash back on all other purchases. Some cards offer even higher cash back percentages for specific gas stations or for buying specific grocery or drug store products.

A quick bit of math will prove how valuable this cash back proposition can be. Let�s say you�re a family of four with two cars. You spend $600 a month at grocery stores, $100 at drug stores, and $200 at gas stations. If you pay for these purchases using your credit card instead of cash or a paper check, that�s $900 per month on which you get 5% cash back. That comes out to $45 per month returned to you. Let�s say that in addition, you use your card to make another $500 in other purchases that qualify for 1% back; that adds another $5 to your coffers, for a total of $50 per month, or $600 per year back to you. Not too shabby for just using a credit card.

Rewards Credit Cards

Some credit cards offer you rewards such as bonus points that count toward gift certificates redeemable at top name stores, such as Best Buy, Home Depot, and Macy�s. Other cards offer you rewards in the form of Frequent Flyer Miles to use on any airline.

Let�s say you use your card to charge $1000 per month on items that you normally would pay cash for. Rather than simply spending your money, now you also get gift certificates to buy merchandise, or frequent flyer miles to tune of 12,000 per year. And some of the cards also offer you a bonus the first time you use the card � so in the case of miles, you can get an extra 15,000 miles, for a grand total of 27,000 miles in one year — enough for a free ticket to anywhere in the US.

Maximizing Your Card Usage

Of course, the key to taking advantage of such cards begins with choosing the one that best fits your normal purchasing habits. Compare online credit card offers and find the offer that makes sense for your lifestyle. If you have a large family and buy lots of groceries, maybe the 5% cash back cards are the best. If you fly often and can benefit from the frequent flier miles, apply for those cards.

Then be sure you maximize your card usage to boost your returns. Use your card everywhere you can. Arrange to pay your regular bills using your credit card, such as your gas and electric utility bills, your doctor and dentist bills — as many regular monthly bills as possible using your credit card.

Still More Amazing — Sign Up Perks

What�s truly mind-boggling is that many banks are also offering great incentives to sign up for their card. You can find offers where you not only will you get cash back and/or rewards, but the bank also has 0% APR financing for 12 months on new purchases and sometimes on balance transfers, and to boot, no annual fee.

All in all, today�s credit card issuing banks are hungry for your business and have become highly competitive in creating promotions to attract you to apply for their card. It is truly impossible to imagine why anyone would not apply to get one of these cash back or rewards credit cards when you have everything to gain, and nothing to lose.

Copyright 2005 Ed Vegliante.

Tinggalkan Balasan