Running a business means making dozens of financial decisions every day. You track expenses, manage cash flow, negotiate contracts, and hunt for margins wherever you can find them. In that environment, a cash back business credit card should not be an afterthought — it can be a smart strategic tool.

Business credit cards don’t just buy office supplies. They shape your liquidity, support growth, and even affect your bottom line. And among them, cash back cards stand out because they deliver real, predictable value — cash that goes straight back into your business.

But here’s the critical insight: cash back cards only work when used intentionally. When used carelessly — like personal credit cards on business expenses — they cost more than they return.

This article explains why cash back business credit cards matter, how they actually work, how to choose the right one, and how smart business owners extract value without falling into common traps.

Why Cash Back Business Cards Matter More Than You Think

Most business owners focus on revenue growth, profit margins, or customer acquisition. Few think deeply about optimizing everyday spending. That’s a mistake — because spending efficiency affects profitability just as much as sales growth.

Cash back business credit cards reward the expenses you already have. They turn spending into returns. This matters because:

- Every dollar saved on cost increases net profit

- Cash flow becomes more flexible

- Rewards can offset overhead and reinvestment

In a world of tight margins, small efficiencies compound.

How Cash Back Business Credit Cards Actually Work

Business credit cards operate similarly to consumer cards, but with features tailored for commercial use:

- Business-specific reporting — easier accounting

- Higher credit limits — support larger spend cycles

- Employee cards with controls — centralized oversight

- Enhanced rewards on common expense categories

On cash back business cards, rewards typically come back as:

- Statement credits

- Direct account deposits

- Reduced annual fees

This real money back improves operational flexibility.

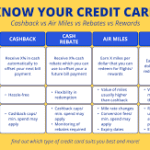

Cash Back Structures: Know Your Options

Cash back business cards tend to follow one of several reward models:

1. Flat-Rate Cash Back

Example: 1.5%–2% on all purchases

Simple. Predictable. Easy to track.

Best for businesses with varied expenses that don’t fit specific categories.

2. Tiered Cash Back

Example: 3% on office supplies, 2% on gas, 1% on everything else

Great when your spending is concentrated in predictable categories.

3. Rotating Bonus Categories

Example: 5% cash back on quarterly categories

High potential value — but requires tracking and activation.

Each structure has trade-offs. The right one aligns with how you already spend, not how you wish you spent.

Top Business Categories that Earn the Most Cash Back

Some common business expense categories that often generate higher rewards include:

- Advertising and marketing

- Office and tech supplies

- Travel (airlines, hotels, rideshares)

- Fuel and transport

- Software and subscriptions

If your monthly spend in these categories is predictable, a cash back card can significantly offset those costs.

Why Business Cash Back Differs from Personal Rewards

A cash back business card is built for operational scale, not discretionary buying:

✔ Separate tax reporting

✔ Easier bookkeeping

✔ Employee spending controls

✔ Higher credit limits

✔ Rewards tied to core business activities

This structure protects both your personal credit and your business’s financial clarity — a crucial advantage for CEOs and founders.

Choosing the Right Cash Back Business Credit Card

Not all cards deliver equal value. Smart business owners evaluate:

1. Reward Rates

Higher cash back on categories you use most.

2. Annual Fees vs Total Value

A fee may be worth it if rewards exceed it.

3. Intro Bonuses

Strong incentives can add immediate value — but only if you spend as part of business operations, not arbitrary purchases.

4. Employee Card Controls

Limits, alerts, and reporting matter for growing teams.

5. Integration with Accounting

Some cards sync with QuickBooks, Xero, or reporting tools — saving time and reducing errors.

The CEO Mindset: Cash Back Is a Financial Lever, Not a Perk

Smart leaders treat card rewards the way they treat pricing, staffing, and growth strategy: as tools, not toys.

They do not:

❌ Spend more just to earn rewards

❌ Mix personal and business expenses

❌ Chase every shiny offer without a plan

They integrate cards into financial strategy:

✔ Earn cash back on planned expenses

✔ Reduce cost of goods sold

✔ Offset fixed overhead

✔ Improve liquidity for investments

This is how rewards translate into measurable business performance.

Avoiding Common Pitfalls

Cash back business credit cards are valuable, but the wrong use can be costly.

Mistake 1 — Carrying a Balance

Interest costs quickly overshadow any cash back earned.

Rule: Pay in full every month.

Mistake 2 — Overspending to Hit Bonuses

Bonuses should follow business activity — not drive it.

Mistake 3 — Mixing Personal and Business Spend

This complicates taxes, accounting, and legal clarity.

Mistake 4 — Ignoring Fees and Terms

Not all bonuses are free money — some come with strings attached.

Discipline turns rewards into profit. Indiscipline turns rewards into debt.

When Cash Back Business Cards Are Especially Smart

These scenarios highlight where cash back cards provide real strategic value:

During Rapid Growth

Higher spend = higher rewards

Reinvest cash back into scaling

When Managing Variable Costs

Rewards cushion unpredictability in fuel, travel, and services

When Planning Large Purchases

Reward bonuses help offset major operational costs

Used intentionally, cash back becomes capital efficiency.

Integrating Cash Back Into Your Financial System

Receiving cash back is not the end — it’s the beginning of a smarter financial workflow.

Smart practices include:

- Categorizing rewards in your budget

- Allocating rewards to reinvestment pools

- Monitoring reward performance quarterly

- Adjusting card usage based on spending trends

This turns passive rewards into active financial optimization.

Final Thoughts: Cash Back Business Cards Are Tools, Not Toys

Cash back business credit cards are not magic. They are strategic financial assets.

In the hands of a disciplined business owner, they:

✔ Improve cash flow

✔ Reduce operating costs

✔ Support financial clarity

✔ Add measurable value every year

But in the hands of someone unfocused, they become:

✖ Expense drivers

✖ Accounting headaches

✖ Risk multipliers

Rewards are real money — but only when used wisely.

Don’t chase offers.

Choose based on strategy.

And let every dollar spent work for your business, not against it.

End of article.

Word Count:

615

Summary:

A typical small business needs to watch every penny. To last in the competitive business world, you need to maximize profits and just as importantly, reduce expenses. Many businesses don�t realize that they could easily be saving a percentage of their purchases with a cash back business credit card. Instead of letting bank fees eat away at your profits, your credit card can work for you.

Keywords:

cash,back,business,credit,card,finance,small,best,rebate,new,compare,choose,choosing,credit card,cards,application

Article Body:

A typical small business needs to watch every penny. To last in the competitive business world, you need to maximize profits and just as importantly, reduce expenses. Many businesses don�t realize that they could easily be saving a percentage of their purchases with a cash back business credit card. Instead of letting bank fees eat away at your profits, your credit card can work for you.

How can the banks offer cash back for your business?

For decades the banks have been charging high interest rates and eating away at business profits. Businesses would just sit back, hoping the bank would eventually give them a better interest rate. Times are changing though. Today the credit card market is very competitive. A business can now choose between credit cards from nearly any financial institution.

As the banks compete, they are offering credit cards with better perks and rewards. If your business needs to travel a lot, you can get airline points. For a business that drives a lot, there are gas station rebate credit cards. Many larger stores even issue their own credit cards with special in store rebates. These credit cards lacked flexibility though. So as competition in the credit card market increased, credit card issuers resorted to offering cash back credit cards.

The banks can afford this to attain a new customer. The cash back is balanced out by interest charges and other fees. So for most people the cash back is just a savings on their bank fees. Plus these same customers might require additional financial services. The banks definitely aren�t losing much money by offering cash back.

Are cash back business credit cards just a scam?

No they are not a scam. These credit cards actually do give your business money back. You just need to be familiar with any restrictions. Most cash back business credit cards have a maximum annual cash back limit. Other cards have different cash back terms based on the credit card purchase type. For example, you might get a different cash back percentage at a gas station compared to a grocery store or office supply store. Some cash back credit cards also have a minimum spending before points can be redeemed.

To get the most out of a cash back credit card, you need to be disciplined. It is very tempting to put extra purchases on your credit card to get more cash back. Only use this strategy if you are able to pay off the card every month. Otherwise you would just be accumulating more interest charges. If you can pay the card off every month, try to use your credit card more instead of cash or checks.

For some businesses the cash back maximum can also be a problem. A business with high operating expenses could easily reach the annual cash back limit in a very short time. If this is the case, consider getting a different credit card to use once the limit has been reached. Some newer cash back business credit cards offer no limit on the amount of cash back you can earn.

Before applying just read the terms and conditions of the credit card. Many cash back credit cards use phrases like �up to 5% cash back�. This usually means that you can only get that cash back percentage for just one type of purchase or there is some other catch.

Despite certain card restrictions, a cash back credit card is a very good idea for your business. Your business could be saving thousands of dollars on your business expenses. Just take the time to compare different cash back business credit card offers before you apply.

Tinggalkan Balasan