Cash is boring.

It doesn’t promise explosive growth.

It doesn’t trend on social media.

It doesn’t come with a success story attached.

And yet, cash quietly remains one of the most powerful tools in personal finance and business decision-making.

In an era obsessed with investing, leverage, and speed, cash often gets dismissed as “idle” or “wasted.” That mindset is not only incomplete—it’s dangerous. Cash plays a role that no other financial asset can fully replace.

This article explains why cash still matters, how smart individuals and executives think about it, and why having cash is not a lack of ambition, but a form of control.

What Cash Really Represents

Cash is not just money sitting in an account.

Cash represents:

- Flexibility

- Liquidity

- Optionality

- Time

When you have cash, you are not forced to act.

When you don’t, every decision becomes urgent.

That difference alone can shape outcomes.

Cash Is Not an Investment—And That’s the Point

One of the most common mistakes people make is judging cash by investment standards.

Cash is not meant to:

- Beat the market

- Generate high returns

- Compound aggressively

Cash is meant to:

- Protect

- Stabilize

- Enable better decisions

Expecting cash to perform like stocks misses its purpose entirely.

Why Cash Becomes More Valuable in Uncertain Times

During periods of volatility, cash does something unique: it gains strategic value.

When markets fall:

- Assets get cheaper

- Opportunities appear

- Risk tolerance drops

Those with cash can move calmly.

Those without it are forced to react—or watch from the sidelines.

Cash doesn’t predict the future.

It prepares you for multiple versions of it.

The Psychological Power of Cash

Beyond numbers, cash changes behavior.

People with adequate cash reserves:

- Take fewer bad risks

- Avoid panic decisions

- Negotiate from strength

- Sleep better

Stress is expensive.

Cash reduces it.

This psychological advantage is often overlooked—but it compounds over time just like returns do.

Cash in Personal Finance: Your First Line of Defense

In personal finance, cash serves as a buffer.

Emergency funds, savings accounts, and liquid reserves exist to:

- Absorb surprises

- Prevent high-interest debt

- Protect long-term investments

Without cash, even small disruptions can derail years of progress.

Cash doesn’t eliminate problems—but it stops them from becoming disasters.

Cash in Business: Oxygen, Not Excess

In business, cash is not optional. It is oxygen.

Companies fail not because they are unprofitable—but because they run out of cash.

Strong cash management allows businesses to:

- Survive downturns

- Pay obligations on time

- Invest strategically

- Avoid desperate financing

Growth without cash control is fragile growth.

Why Smart Investors Still Hold Cash

Even experienced investors keep cash—intentionally.

They understand that:

- Timing matters

- Liquidity creates opportunity

- Forced selling destroys value

Cash is not a permanent position.

It is a tactical one.

The goal is not to hold cash forever—but to have it when it matters.

The CEO Mindset: Cash Buys Time

Executives value time more than excitement.

Cash buys time to:

- Think clearly

- Evaluate options

- Wait for better conditions

- Say no to bad deals

In leadership, the ability to delay a decision is often as powerful as the ability to act quickly.

Cash enables that choice.

The Cost of Ignoring Cash

People who ignore cash often experience:

- Overleveraging

- Forced asset sales

- Missed opportunities

- Constant financial pressure

Being “fully invested” sounds efficient—until flexibility is needed.

Efficiency without resilience is fragile.

Finding the Right Balance

Holding too much cash can reduce long-term growth.

Holding too little increases vulnerability.

The right balance depends on:

- Income stability

- Risk tolerance

- Time horizon

- Life stage

The key is intention.

Cash should be held by design—not by accident or fear.

Final Thoughts: Cash Is Quiet Power

Cash will never be glamorous.

But it doesn’t need to be.

It protects you when things go wrong.

It positions you when things go right.

And it gives you control when others feel trapped.

In finance, power rarely announces itself loudly.

Sometimes, it just sits there—ready.

That’s cash.

End of article

Summary:

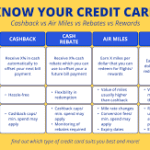

When considering a reward credit card, most people prefer to get a cash back credit card. This is because, cash back credit cards provide more options and flexibility for the card holder. While not everyone frequently travels and not everyone drives his own car, cash back cards have become more popular than Frequent Flyer Miles credit cards and Gas Rewards credit cards.

Keywords:

cash back credit cards,cash back credit card,credit card cash back,cash back credit card offers,business credit card cash back,cash rebate credit card

Article Body:

When considering a reward credit card, most people prefer to get a cash back credit card. This is because, cash back credit cards provide more options and flexibility for the card holder. While not everyone frequently travels and not everyone drives his own car, cash back cards have become more popular than Frequent Flyer Miles credit cards and Gas Rewards credit cards.

Cash back credit cards give card holders their incentive in terms of cash or money points. Each time the card holder makes a purchase, the purchase amount has a corresponding cash amount that can be used to make new purchases or pay other bills. For this reason, anyone can be an ideal candidate for a cash back card.

Making the Choice

Every credit card issuer offers its own cash back program. Obviously, each cash back credit card also has its own terms and conditions to follow. Knowing this, everyone is advised to take their time in researching about these terms and comparing each credit card from the other.

Today, you can find review sites that are exclusively dedicated to providing reliable credit card reviews for consumers. Usually, these sites are categorized according to the type of credit card you�re looking for. For instance, if you�re looking for a cash back credit card, you should check out the page that is focused on reviews about the different cash back cards in the market. Through these review sites, comparing credit cards become easier. Once you�ve narrowed down your choices, based on the reviews you�ve read from the site, then you can start visiting the credit card�s official website for further examination.

Not all about the APR

One of the first things you need to check on is the APR or in the Annual Percentage Rate. Since most reward credit cards are accompanied with high interest, you�ll want to search for one with the lowest or most reasonable rate. Still, the interest rate is not the only cost associated with your credit card.

Don�t focus your attention the cash back card�s interest rate alone. Some credit cards may offer an incredibly low interest rate as part of its introductory offer but the other costs and charges can take you by surprise. Always check on the exact cost of all fees that you�ll be paying. For instance, how much is the annual fee? Is it reasonable enough or would you be paying for an expensive activation fee every year? How much are the penalty charges? Don�t forget to examine each fee that comes with your card and make sure that all fees are reasonable.

Earning and Redemption

Okay, so you�ve checked on the fees and costs. You�ve checked on features. Everything sounds great. But have you checked on the rules of the rewards? Are you clearly aware of the procedures on how you can earn points? What about the steps in claiming the rewards? Is there an expiration period or blackout date on your card? Remember to take your time in studying the regulations of the credit card�s reward system before making your decision.

Tinggalkan Balasan